When you pick up a prescription at the pharmacy, you might not realize that your out-of-pocket cost isn’t just about the drug-it’s shaped by a hidden system called a formulary. Most employer-sponsored health plans use tiered formularies to decide which drugs cost you $10, $40, or even $200. And in nearly every case, generics are the cheapest option-not because they’re less effective, but because the system is designed to push them hard.

Why Generics Are the Default Choice

The FDA confirms that generic drugs are just as safe and effective as brand-name versions. They contain the same active ingredients, work the same way, and meet the same quality standards. The only real difference? Price. Generics cost 80-85% less because manufacturers don’t have to repeat expensive clinical trials or run billion-dollar ad campaigns. That’s why employers and their pharmacy benefit managers (PBMs) push generics so hard. In 2023, generic medications saved the U.S. healthcare system over $150 billion in a single year. That’s $3 billion every week. For employers, that’s not just a nice saving-it’s a necessity. Rising drug costs are one of the biggest drivers of premium increases. By steering employees toward generics, companies can keep health plans affordable for everyone.How Tiered Formularies Work

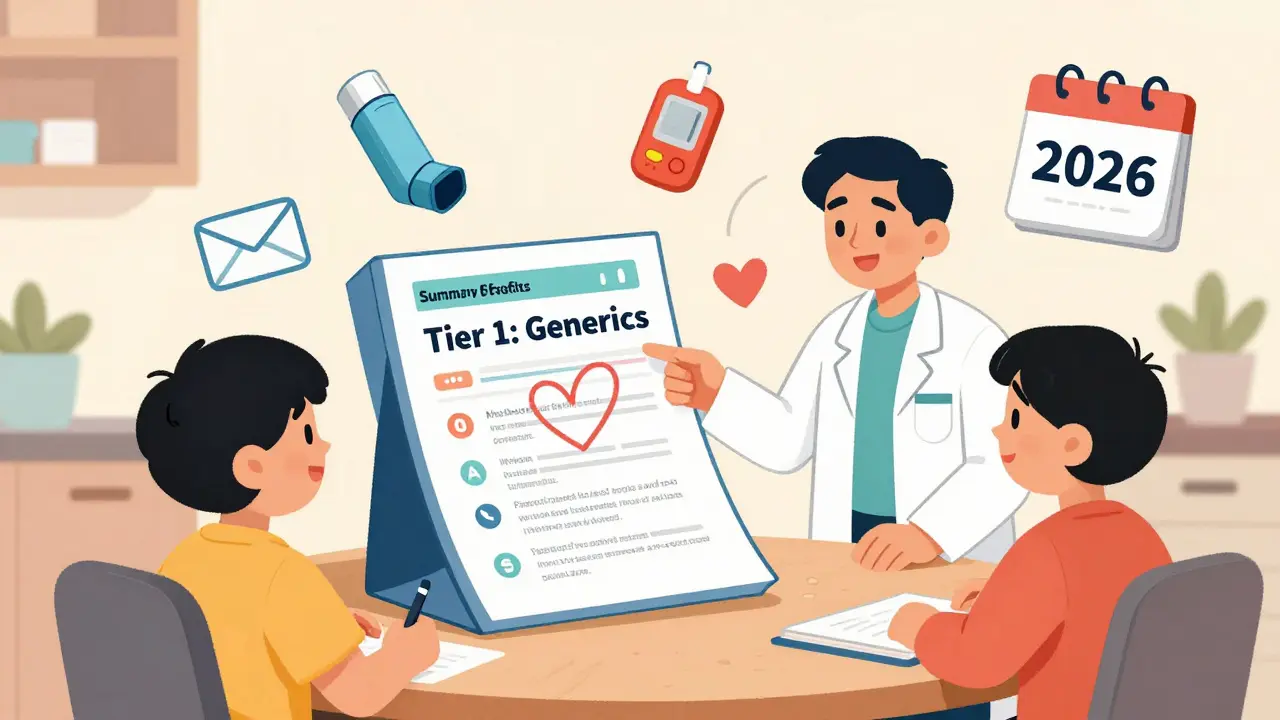

Most employer plans divide drugs into four tiers:- Tier 1: Generics - Usually $10 or less per prescription

- Tier 2: Preferred brand-name drugs - Around $40

- Tier 3: Non-preferred brand-name drugs - Typically $75

- Tier 4: Specialty drugs - Often hundreds of dollars, sometimes requiring prior authorization

What Happens When Your Drug Gets Removed

In January 2024, each of the three largest PBMs removed more than 600 drugs from their formularies. That’s over 1,800 medications pulled in a single month. Why? To pressure drugmakers into giving bigger rebates. This is called a “formulary exclusion.” If a manufacturer won’t offer a deep enough discount, the PBM simply won’t cover the drug anymore. The result? You can’t get it through your plan unless you pay full price-or your doctor files a medical exception. Let’s say you’ve been taking a brand-name asthma inhaler for years. One day, you go to refill it and find it’s no longer on the formulary. Your plan won’t pay for it. You have three options:- Switch to a generic or preferred alternative (if one exists)

- Pay out of pocket-sometimes hundreds of dollars per month

- Ask your doctor to request a coverage exception

Why You Might Not See the Savings

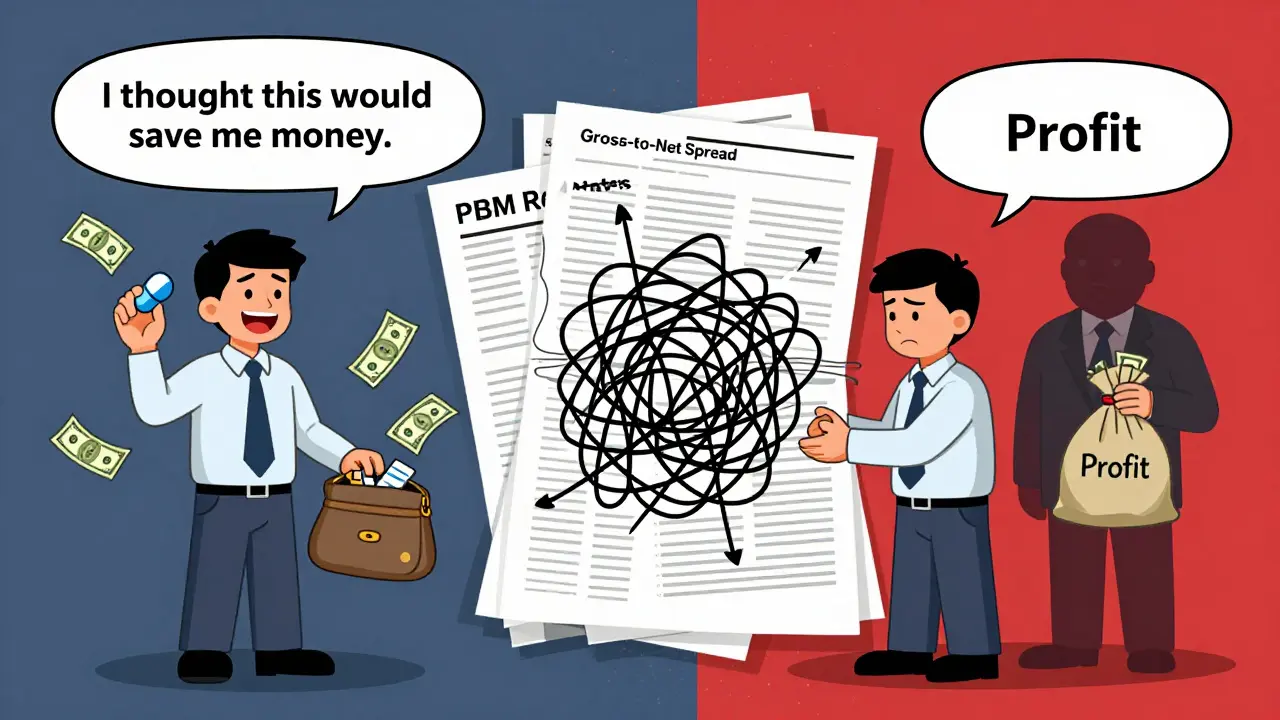

Here’s the twist: the money saved from generics and formulary exclusions doesn’t always go to you. PBMs use a pricing model called gross-to-net (GTN). A drug might have a list price of $100, but after rebates, discounts, and returns, the PBM pays only $45. That 55% difference? That’s the GTN spread. KPMG found that average in 2023. The problem? PBMs often keep a big chunk of those rebates. Instead of lowering your copay, they use the savings to boost their own profits. So even though your plan saves $150 billion a year on generics, your $10 copay might not drop to $5. You’re not seeing the full benefit. Scott Glovsky, a healthcare analyst, calls this a “disconnect.” The system is designed to save money-but not necessarily to save you money.What You Can Do to Save Money

You don’t have to accept whatever your plan throws at you. Here’s how to take control:- Check your formulary - Go to your insurer’s website and search for your medication. Look for the tier and copay. If it’s not listed, it’s not covered.

- Ask about generics - If your doctor prescribes a brand-name drug, ask: “Is there a generic version?” Many don’t realize generics exist.

- Use in-network pharmacies - Some plans, like HealthOptions.org’s Price Assure Program, automatically lower the cost of generics at in-network pharmacies. Out-of-network? You could pay double.

- Call your insurer - Don’t rely on your employer’s HR portal. Call your plan directly. Ask: “Is this drug on the formulary? What’s my copay? Is there a preferred alternative?”

- Review your Summary of Benefits - This document, required by law, explains your drug coverage. Look for the “Prescription Drugs” section. It will show you tiers, limits, and exceptions.

What Employers Should Be Doing

Employers aren’t just paying for coverage-they’re shaping health outcomes. The best ones don’t just hand out a benefits brochure and walk away. They educate. Schauer Group found that many employees would use generics-if they understood they were safe and cheaper. But too many believe generics are “weaker” or “old drugs.” That’s misinformation. Employers can fix this with simple, clear messages:- Emails explaining how generics work

- Payroll stuffers with real cost comparisons

- Short videos from pharmacists

- One-on-one help from care managers

Paul Ong

1 January, 2026 . 17:36 PM

Just got my diabetes med switched to generic and my bill dropped from $85 to $12. No joke. I thought they were sketchy but turns out my blood sugar’s actually more stable now. Weird how the system hides this stuff

Phoebe McKenzie

1 January, 2026 . 23:56 PM

Of course the PBMs are stealing. They’re corporate vultures. The government lets them loot billions while we’re stuck paying $40 for insulin that costs $2 to make. This isn’t healthcare it’s a rigged casino and you’re the sucker

Andy Heinlein

3 January, 2026 . 02:43 AM

whoa i just checked my formulary and my asthma inhaler is tier 4 now?? i thought i was safe lol guess i gotta call my doc before next refill

Stephen Gikuma

3 January, 2026 . 08:57 AM

Big Pharma and PBMs are in bed together. This is all a scam to make you dependent on their drugs while pretending they care about your health. You think this is about savings? Nah. It’s about control. The same people who run your insurance own the drug companies. Watch the news

sharad vyas

4 January, 2026 . 20:57 PM

In India we have generics everywhere. They are not cheaper because they are bad. They are cheaper because we don’t waste money on ads. A medicine is a medicine. If it works, it works. Why do we need to pay for marketing?

gerard najera

6 January, 2026 . 01:22 AM

Generics work. Formularies are arbitrary. PBMs profit. You pay the difference.

LIZETH DE PACHECO

7 January, 2026 . 15:27 PM

My mom had a heart condition and they switched her meds to generic without telling her. She was terrified at first but after two months her doctor said her numbers were better than ever. Don’t fear generics. Ask questions. You got this

Layla Anna

8 January, 2026 . 14:36 PM

OMG I had no idea about the GTN spread 😭 I just thought my copay was high because I’m unlucky. This explains so much… thanks for sharing this

Bobby Collins

10 January, 2026 . 11:22 AM

they’re watching us. every time you switch to a generic they log it. next thing you know your premiums go up because you’re ‘low risk’ and they want to charge you more to make up for it. trust no one

Austin Mac-Anabraba

10 January, 2026 . 20:18 PM

The entire system is a grotesque misalignment of incentives. Employers outsource cost control to PBMs who prioritize rebate extraction over patient outcomes. The result is not efficiency-it’s institutionalized exploitation masked as fiscal responsibility. This isn’t capitalism. It’s predatory rent-seeking.

Heather Josey

12 January, 2026 . 05:26 AM

If your employer offers a Chronic Illness Support Program, please take advantage of it. I’ve seen people save hundreds a month just by talking to a care manager. It’s not complicated-just ask. You deserve to understand your coverage.

Donna Peplinskie

13 January, 2026 . 01:23 AM

Thank you so much for writing this-it’s so easy to feel lost in all this, but now I know where to look! I’m going to check my formulary tonight and maybe even share this with my coworkers… we all need to know this stuff!